A Journey to Compliance, Courage, and Clarity

Inspired by The Wizard of OZ and The Wiz

Alexander Christian · AML Compliance Services · London · alexanderchristian.co.uk

2027 is closer than it looks. The FCA is expected to take over AML supervision of law firms from the SRA, with the FATF mutual evaluation scheduled for August 2027. Small law firms in London that have not yet reviewed their AML frameworks have less time than they may think. This post explains why — and what to do about it.

Ai Conversation about this blog post

Click the button to stop or start

- AML Through the Emerald Lens_ The Yellow Brick Risk Road.wav00:00

"Ease on down, ease on down the road." The Wiz got a lot of things right. And in the world of AML compliance for small law firms, the message holds: the journey matters as much as the destination. But unlike Dorothy, who only had to get to the Emerald City once, AML compliance is not a destination. It is an ongoing journey — one that, in 2025 and beyond, is changing direction significantly.

This post is written for small law firms in London navigating the requirements of the Money Laundering, Terrorist Financing and Transfer of Funds (Information on the Payer) Regulations 2017 (the MLRs) — and preparing for the supervisory landscape that is coming. It uses the characters and moments from Oz as a framework for something entirely real: the compliance journey that every regulated firm is on, whether they know it or not.

There is no yellow brick road in AML compliance. But there is a clear path — and the firms that follow it with genuine commitment tend to arrive in a much better position than those who are still looking for it when the inspector calls.

🎭 Setting the Stage — The Land of AML

The UK legal sector operates in one of the most heavily scrutinised AML environments in the world. Law firms are relevant persons under the MLRs, which means they carry specific statutory obligations — not optional best practices, but legal requirements. Failure to comply is not just a regulatory risk. It is, in serious cases, a criminal one.

For small law firms in London, those obligations can feel overwhelming. The guidance is extensive. The acronyms proliferate.

The regulatory expectations have grown significantly since the MLRs came into force in 2017, and they are growing further still as the supervisory landscape is restructured ahead of the 2027 FATF mutual evaluation.

The SRA's AML Annual Report 2024-25 made the picture clear: the regulator found AML failings in the vast majority of firms it reviewed. Not through deliberate wrongdoing, but through frameworks that were incomplete, risk assessments that were inadequate, and training that had not kept pace with the requirements. The firms that struggled were not rogue operators. They were ordinary, hardworking practices that had not given their AML obligations the structured attention they required.

This is a journey every firm is on. The question is whether they are walking it with their eyes open.

This is a journey every firm is on. The question is whether they are walking it with their eyes open.

👧🏻 Dorothy — The Compliance Officer or MLCO

Dorothy arrives in a strange land with limited preparation, a set of rules she is still learning, and an urgent need to find her way home. She is not the villain. She is not incompetent. She is simply in a situation she did not entirely expect, trying to navigate it with the tools she has.

The compliance officer or MLCO in a small London law firm often finds themselves in exactly this position. The role exists. The obligation to have a nominated officer exists. But the support, training, and structured framework that would make that role genuinely effective? That is what the journey is for.

Under the MLRs, the MLCO is responsible for the firm's compliance with the regulations — including the firmwide risk assessment (FWRA) under Regulation 18, the policies, controls and procedures (PCPs) under Regulation 19, ongoing monitoring, staff training, and the escalation of suspicious activity to the Money Laundering Reporting Officer (MLRO). These are statutory requirements, not guidance notes.

AML Lesson

The answers were always within reach — but they require the right guidance, the right training, and the courage to act on what is found. Compliance does not require perfection. It requires genuine, documented, proportionate effort. The firm that can demonstrate it has thought carefully about its risks and taken reasonable steps to manage them is in a fundamentally different position from the one that cannot.

🦁 The Cowardly Lion — The Nervous MLRO

The MLRO is the person to whom all internal suspicious activity reports (SARs) are escalated — and the person who decides whether to submit an external SAR to the National Crime Agency (NCA). It is a role that carries significant personal responsibility, and with that responsibility can come significant anxiety.

The Cowardly Lion knows what courage is required. He feels the weight of the decision. He worries about getting it wrong — about submitting a SAR when he should not, or failing to submit when he should. He worries about what happens if he challenges a partner, or declines a client, or raises a concern that makes him unpopular.

That anxiety is understandable. The MLRO's role sits at the intersection of legal obligation, professional relationship, and personal liability. Under Regulation 21, the firm is required to ensure that its MLRO has the necessary skills, experience and resources to discharge their responsibilities effectively. That is not a box-ticking exercise — it means genuine, documented competence, not just a job title.

A SAR not submitted when it should have been is not a minor oversight. It is a potential breach of section 330 of the Proceeds of Crime Act 2002 — the failure to disclose. That is a criminal offence.

AML Lesson

True courage is not the absence of anxiety. It is the ability to act responsibly in the presence of it. The MLRO who has the right training, the right support, and a clearly documented decision-making framework can make difficult calls with confidence — not because the calls are easy, but because the framework makes the right answer clearer. If the MLRO in your firm is working without that framework, that is a compliance gap.

🤖 The Tinman — The Firm That Ticks Boxes Without Thinking

The Tinman has all the right components. He moves. He functions. He follows the sequence. What he lacks is the heart that makes the process meaningful — the genuine understanding of why each step matters, the culture of compliance that makes the right thing the natural thing.

The SRA has been clear, and its annual reports make this explicit: the most common AML failing in small law firms is not the absence of documentation. It is the absence of genuine implementation. The firmwide risk assessment exists but has not been reviewed since it was produced. The client risk assessment template is in the system but the fee earners do not know how to use it. The training has been completed but the learning has not been applied.

This is the compliance that looks right on paper and fails in practice. It is precisely what a Regulation 21 audit is designed to detect — not just whether the policies exist, but whether they are working. Whether the controls are effective. Whether the recommendations from previous reviews have been actioned.

AML Lesson

Compliance needs more than forms. It needs a culture — a genuine understanding across the firm, from the principal to the newest fee earner, of what the requirements are and why they exist. The LSAG guidance is explicit on this: AML must be embedded in the way the firm operates, not appended to it. Tick-box compliance is not compliance. It is the illusion of compliance — which, as any visitor to the Emerald City eventually discovers, is not the same thing at all.

🧠 The Scarecrow — The Overwhelmed Fee Earner

The Scarecrow is not lazy. He is not indifferent. He wants to help. He simply does not have the knowledge and framework that would allow him to do so effectively. He is standing in a field of regulatory complexity, aware that something is required of him, uncertain what it is.

This is the most common experience for fee earners in small law firms when it comes to AML. They are aware of the requirements in general terms. They know they need to carry out client due diligence (CDD). They know they need to identify and verify clients. They are less certain about what enhanced due diligence (EDD) looks like in practice, when simplified due diligence (SDD) is appropriate, what a client risk assessment should contain for their particular type of matter, and when they need to escalate something to the MLRO.

The SRA's AML Controls Webinar from March 2026 reinforced this consistently: the common failures are not in the existence of procedures but in the application of them — fee earners who do not know what the firmwide risk assessment says, who are applying standard CDD to high-risk matters, who have never been shown what an adequate matter-level risk assessment looks like for the work they are doing.

AML Lesson

With the right training — specific, practical, and tailored to the firm's own policies and the type of work it does — even the most uncertain fee earner can become a genuinely effective participant in the firm's AML framework. The Scarecrow did not lack a brain. He lacked the confidence that came from knowing he had one. Good AML training does the same thing: it does not give fee earners knowledge they did not have. It gives them confidence in applying what they already know, and clarity about where to turn when they are unsure.

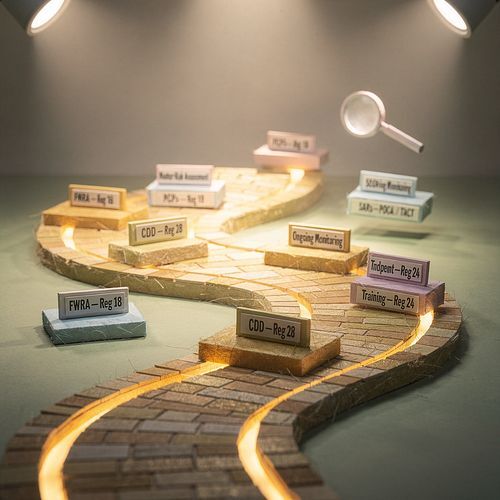

The Yellow Brick Risk Road — Your Compliance Journey Under the MLRs

The Money Laundering Regulations 2017 set out a risk-based framework. That means the obligations are not uniform — they are proportionate to the risks the firm faces. But proportionality does not mean minimal. It means genuinely calibrated to your specific risk profile, documented clearly, and applied consistently.

The bricks you cannot afford to skip

Firmwide Risk Assessment (FWRA) — Regulation 18

The foundation of the entire framework. The FWRA requires the firm to identify and assess the money laundering, terrorist financing, and proliferation financing risks it faces across its operations — by client type, service type, geographic exposure, and delivery channel. The SRA's template is a starting point, not the answer. Your FWRA must reflect your actual practice. It must be kept up to date. It must be the document your fee earners actually use.

Client Due Diligence (CDD) — Regulation 28

Know your client — not just their name and address, but who they are, what they do, the nature of the business relationship, and the purpose of the matter. Standard CDD applies to most clients. Simplified due diligence (SDD) is available only in limited, documented circumstances. Enhanced due diligence (EDD) is required for higher-risk clients and situations — including politically exposed persons (PEPs), high-risk third countries, and complex or unusually large transactions. Ask questions. Challenge responses. Dig deeper.

Client and Matter Risk Assessment — Regulation 28

The FWRA sets the firm's overall risk profile. For each individual client and matter, a separate risk assessment must be carried out — considering the specific risk factors of that client, that matter, and that transaction. These are not the same document. Failing to complete matter-level risk assessments is one of the most commonly cited failures in SRA reviews. The client risk assessment must inform the level of CDD applied.

Policies, Controls and Procedures (PCPs) — Regulation 19

The firm must have written policies, controls and procedures covering all areas of its AML obligations. These must be proportionate to the nature and size of the firm, kept up to date, and communicated to all relevant staff. PCPs that sit in a drawer are not PCPs — they are documents. The distinction matters, and the SRA makes it consistently.

Ongoing Monitoring — Regulation 28(11)

CDD is not a one-off exercise. The firm must conduct ongoing monitoring of its business relationships — including scrutiny of transactions and keeping CDD documents and information up to date. For higher-risk clients this must be more frequent and more thorough. The trigger for updating CDD is not just time: it is any change in the client's circumstances, the nature of the matter, or the risk profile of the relationship.

Suspicious Activity Reporting — POCA 2002 / TACT 2000

Where a relevant person knows or suspects — or has reasonable grounds to know or suspect — that a person is engaged in money laundering, there is an obligation to submit a SAR to the NCA via the Suspicious Activity Reports regime. The failure to report is a criminal offence under section 330 of POCA 2002. The consent / information SAR — where the firm seeks a defence against money laundering before proceeding — has specific procedural requirements. The MLRO must be equipped to make these decisions with confidence.

Training — Regulation 24

All relevant employees must receive regular AML training — appropriate to their role, their level of responsibility, and the risks the firm faces. Training must be documented. It must be more than a generic online module completed once a year. It must address the firm's specific policies, procedures, and risk profile — and it must be updated when those things change.

Independent Audit — Regulation 21(1)(c)

Firms must examine and independently audit the adequacy and effectiveness of their AML framework on a regular basis and — critically — act on the recommendations that audit produces. The independence requirement is significant: an audit conducted by the same person responsible for the framework being audited does not meet the requirement. For small firms where internal independence is structurally impossible, external audit is the answer.

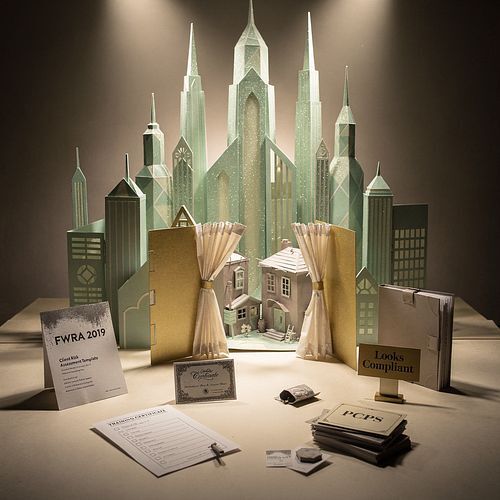

💚The Emerald City – The Illusion of Compliance

The Emerald City gleams from a distance. It looks exactly as it should. It is only when Dorothy and her companions arrive — and pull back the curtain — that the reality becomes visible. Behind the spectacle is something considerably more modest than the promise.

In AML compliance, the Emerald City is the firm that has the documentation without the implementation. The FWRA that was produced in 2019 and has not been reviewed since. The client risk assessment template that was purchased from a legal publisher and applied uniformly regardless of the actual risk of the matter. The training certificates in the file and the fee earner who cannot explain what the firm's CDD procedures require.

Real compliance is not built on glitter. It is built on documented, proportionate, genuinely implemented frameworks — and on the demonstrated ability to explain, evidence, and defend every decision when the regulator asks.

The SRA has been increasingly explicit about this distinction. In its AML Annual Report 2024-25, it recorded that while most firms had documentation in place, the proportion whose documentation was effectively implemented and regularly reviewed was considerably smaller. The gap between having a policy and running a compliant practice is where most enforcement action lives.

The Regulation 21 independent audit exists precisely to close that gap — to provide an objective, external assessment of whether the framework is not only adequate in design but effective in operation.

🗺 The Road Ahead — 2027 and the FCA Transition

For small law firms in London, the compliance landscape is about to change more significantly than at any point since the MLRs came into force in 2017. Understanding what is coming — and why the time to act is now — is not optional

FCA to become single AML supervisor for law firms

The UK Government announced in October 2025 that the Financial Conduct Authority (FCA) will take over AML/CTF supervision of law firms from the SRA and other professional body supervisors. This is not a minor adjustment to an existing system. It is a fundamental restructuring of how legal sector AML compliance is supervised in the UK.

The driver is the FATF mutual evaluation scheduled for August 2027 — at which the UK must demonstrate a credible, consistent, and effective supervisory system. The existing fragmented model, with 22 supervisors across the legal and accountancy sectors, has been assessed as inadequate for that purpose. The FCA's single-supervisor model is the government's response.

For small law firms currently supervised by the SRA, this means a transition from a sector-specific, guidance-led regulator to a supervisor whose enforcement culture is considerably more intensive.

The FCA has issued penalties running to tens of millions of pounds. The expectations around governance, risk assessment, monitoring, and controls are higher — and the consequences of falling short are more significant.

HM Treasury announces FCA to become single professional services AML supervisor. Consultation launched on powers, duties and accountability mechanisms.

King's Speech expected to announce new AML Supervision Bill.

Draft legislation setting out FCA's expanded remit expected to be published.

Bill expected to receive Royal Assent. FATF mutual evaluation of the UK's AML supervisory system.

Preparatory and transition phases — registration, fit and proper assessments, publication of new AML Handbook.

Full implementation of FCA supervision across all in-scope professional services firms, including law firms currently supervised by the SRA.

What this means for small London law firms right now

The transition to FCA supervision does not remove the current obligations under the MLRs 2017. Every requirement that applies today — firmwide risk assessment, client and matter risk assessments, CDD, ongoing monitoring, training, independent audit — continues to apply throughout the transition period and beyond.

What the transition does is raise the stakes for non-compliance. A firm that arrives at FCA registration with an inadequate or unreviewed AML framework will be starting a new supervisory relationship from exactly the wrong position. The FCA's approach to supervision is more intensive, its enforcement powers are more significant, and its expectations around documented effectiveness are higher than those of the SRA.

The most effective preparation for any future supervisory regime is to ensure that the current framework is fully compliant, genuinely implemented, and regularly reviewed. That is true regardless of who the supervisor is. It is especially true in the period immediately before a significant change in who that supervisor will be.

🎶 Final Message:

"Ease on down, ease on down the road."

The spirit of The Wiz is right: AML compliance does not have to be approached with dread. It can be approached with purpose, with structure, and with the genuine confidence that comes from knowing your framework is sound.

But easing on down is not the same as easing off. The firms that navigate the compliance journey well are not the ones who treat it as a burden to be minimised. They are the ones who treat it as a professional obligation — one that, done properly, protects their clients, protects their practice, and protects the individuals within it who carry personal responsibility for the firm's compliance.

The yellow brick road has a destination. In AML compliance, that destination is not a wizard who can give you what you already have. It is the clear, documented, genuinely effective framework that the regulations require — and the confidence that comes from knowing, when the inspector calls, that your house is in order.

The firms that will fare best under FCA supervision are the ones that are already compliant under the current regime — not because they anticipate the change, but because they have taken their existing obligations seriously.

How Alexander Christian can help

AML Compliance Services for Small London Law Firms

Alexander Christian provides independent AML compliance support for small law firms in London,

Regulation 21 Independent Audit

A formal independent audit of your firm's AML framework — examining adequacy, effectiveness, and compliance with recommendations. Produced to the standard required for regulatory purposes.

AML File Reviews

A structured review of client files against your firm's policies, controls and procedures — identifying gaps in CDD, risk assessment, and ongoing monitoring at the matter level.

Mock AML Audit

An informal audit that goes through the rigours of the formal process — giving you a clear picture of where attention is needed before the regulator asks the same questions.

Staff Interviews

Assessment of how AML policies are understood and applied across the firm — examining training effectiveness, escalation, SAR awareness, and compliance culture.

🏆Credit and Copyright

Lyman Frank Baum

The Musical and Film - The Wizard of OZ

The Musical and Film - The Wiz

And all contributors - no copyright infringement intended.

Educational usage only.

Disclaimer

The contents of this post are not legal or regulatory advice and are not intended to be considered as such.

Always seek independent legal or regulatory advice from a provider who is qualified to provide such.

We exclude all liability.

See our Disclaimer